Industry

Vol. 1·Wednesday, March 25, 2026

Venture Capital Has a Ten-Company Problem

Noah Ogbi8 min read

Tips, corrections, or questions? support@omniscient.media

TopicsIndustry Strategy

Tips, corrections, or questions? support@omniscient.media

Consequential AI, explained and evaluated, every weekday.

The Omniscient Bulletin: 5 to 7 items a day with the take, not the recap.

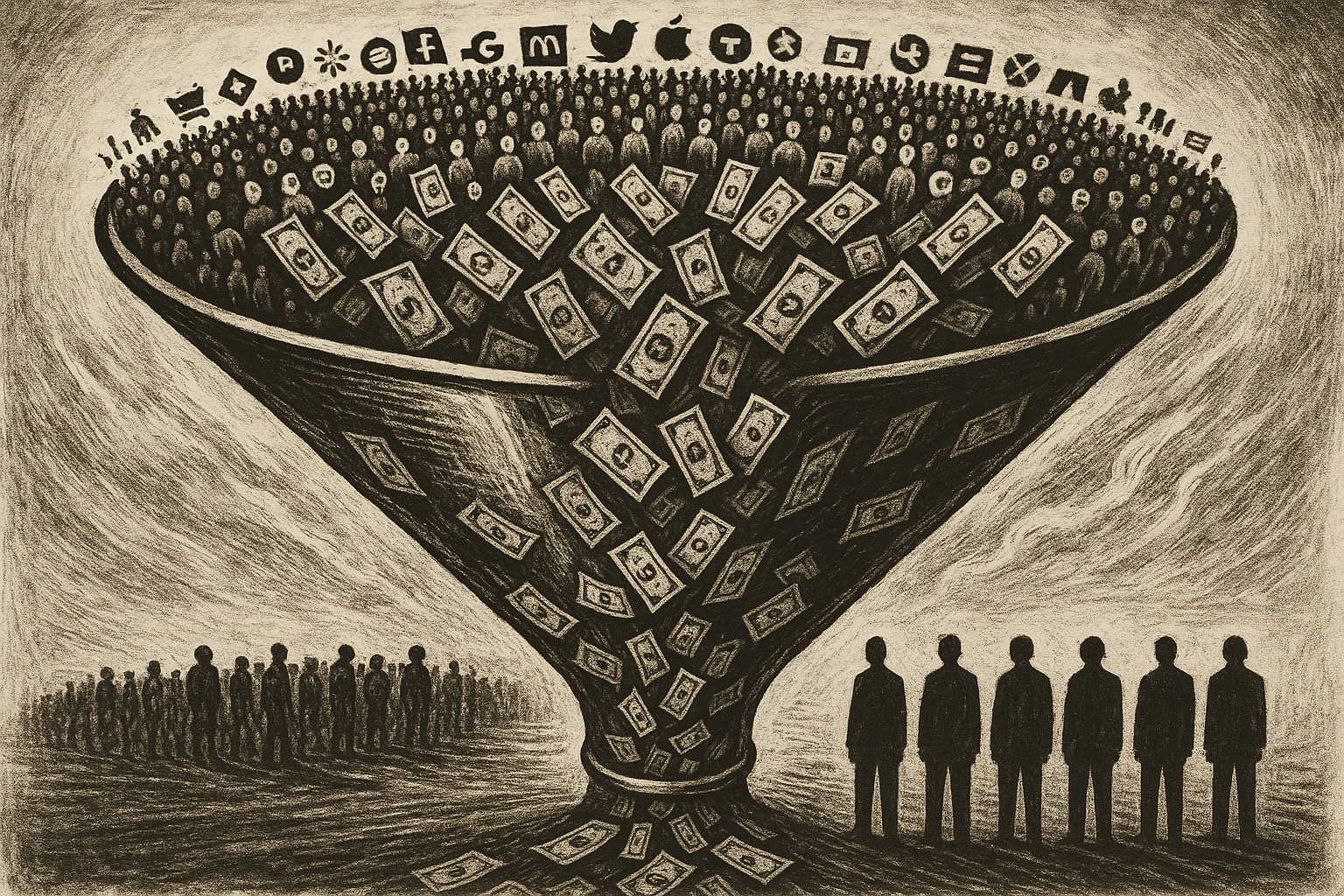

Venture capital has always operated on power-law logic: a handful of outsized winners subsidize the losses across a portfolio. What happened in 2025 is something categorically different. According to PitchBook data, just ten companies absorbed 41% of all venture dollars deployed in the United States - $81.3 billion out of $197.2 billion total - the highest concentration recorded in at least a decade.[1] Eight of those ten companies are AI-focused. That 41% share represents a 75% increase over the top-ten concentration figure from 2024 alone - not a gradual drift but an acceleration.[1]

The individual figures are extraordinary in their own right. OpenAI's $40 billion financing in Q1 was the largest single venture event in history; the top three AI companies by capital raised - OpenAI, xAI, and Anthropic - collectively drew $65 billion, roughly one dollar in three of everything deployed in the U.S. that year.[1] Zoom out globally and the picture remains striking: PitchBook's full-year data puts total deal value at $512 billion, the second-highest annual figure on record, with AI accounting for more than half.[2] By almost every aggregate measure, 2025 looks like a boom. The problem is that aggregates are doing an unusual amount of concealment this cycle.

Strip out the mega-rounds and 2025 looks less like a boom than a triage. Carta's analysis of over 60,000 startups on its platform recorded just 4,859 new funding rounds for the full year - a six-year low, down 41% from the 2021 peak - even as total capital raised climbed 17% to $119.5 billion.[3] More capital concentrated into fewer companies is not the same thing as a healthy market; it is the signature of a market sorting itself into tiers with diminishing connectivity between them. Seed funding fell 14% year-over-year in early 2025, with early-stage investment dropping to its lowest level in at least five quarters.[1]

The valuation data Carta published makes the bifurcation mechanism visible. At Series A, the median AI startup commanded a valuation 38% above its non-AI peer. By Series E and beyond, that premium had expanded to 193%.[3] The gap does not simply reflect AI companies being better businesses - it reflects a self-reinforcing capital dynamic in which perceived category dominance attracts money that further entrenches dominance. Sectors that require long development horizons and patient capital - climate tech, biotech, infrastructure - are structurally disadvantaged in this environment. Investors surveyed by Crunchbase specifically named climate tech and vertical SaaS without AI differentiation among sectors expected to lose share of venture dollars in 2026.[4]

The three largest AI financings of 2025 share an architecture that has no equivalent in standard venture practice. Each bundles equity with commitments that serve the strategic interests of the investing corporation as directly as they serve the portfolio company. Meta's $14.3 billion investment in Scale AI secured a 49% non-voting stake while installing Alexandr Wang - Scale's founder - as Meta's first-ever Chief AI Officer leading its new Superintelligence Lab: a single transaction that simultaneously bought equity, acquired specialized data-labeling capability, and repositioned a rival's founding talent inside Meta's own research hierarchy.[1] Amazon's cumulative $8 billion commitment to Anthropic included an agreement that Anthropic designate AWS as its primary cloud provider - turning a financing into a distribution and infrastructure contract simultaneously.[1] Microsoft's arrangement with OpenAI weaves together equity, compute access, and product integration rights in ways no traditional term sheet would accommodate.

The common thread is that the strategic value flowing back to the investor - cloud revenue, platform lock-in, talent capture, roadmap influence - is load-bearing in each deal's logic. These are not bets on an independent team finding product-market fit against an open competitive field. They are incumbents acquiring structural position in the next platform layer under the legal form of a minority investment. Counting them alongside a $5 million Series A in the same "venture deployment" aggregate is a category error that flatters both the health of the market and the risk appetite of its largest participants.

The implication for the concentration data is significant. A meaningful share of that $81.3 billion flowing to the top ten is not risk capital in the traditional sense - it is defensive spend by hyperscalers protecting cloud and compute franchises whose economic value dwarfs any venture return. When that capital is included in the denominator of "venture health," the picture it produces is misleading.

The most telling indicator in PitchBook's full-year report attracted almost no coverage: global VC fundraising - the dollars flowing from limited partners into venture funds - fell to $118.6 billion in 2025, the lowest level in a decade and nearly $100 billion below 2024.[2] The number of newly closed funds reached a ten-year low as well, at 537, compared with 1,777 in 2022.[2] The deployment surge and the fundraising collapse are happening simultaneously, which means the former is being financed by existing dry powder held at established mega-funds - not by fresh LP conviction in the asset class. First-time fund managers raised a combined $1.8 billion across 44 funds in 2025, less than half the $4.6 billion Founders Fund alone raised in the same period.[1]

The liquidity picture compounds this. Global VC exit value reached $549.2 billion in 2025, up more than $200 billion from 2024 - but the number of completed IPOs actually declined year-over-year, with aggregate exit figures propped up by a handful of high-profile listings rather than a broad reopening of public markets.[2] Carta recorded 396 tender offers during 2025 - up 62% from 2024 - with nearly 20% originating from companies at Series E or later.[3] Late-stage shareholders are not waiting for an IPO window that has not reopened at scale; they are manufacturing liquidity privately, a sign that the exit environment is more constrained than headline exit-value figures suggest.

The honest answer is that these two diagnoses are not in competition. A genuine technological transition - one with real consequences for how software is built, how knowledge work is organized, and how compute is priced - can run in parallel with a valuation structure that has outpaced underlying economics. The internet was both genuinely transformative and, for several years, catastrophically mispriced. The current moment has a reasonable claim to the same dual character.

What is harder to explain away is the speed of the gravitational collapse. A 75% increase in top-ten concentration in a single year is not a market maturing toward efficiency - it is capital making fewer and larger bets as uncertainty increases, not fewer because the field has narrowed to proven winners.[1] The companies absorbing the bulk of deployment are not post-revenue businesses with demonstrated unit economics; most are pre-profitability infrastructure bets whose returns remain speculative over any reasonable investment horizon. The market is funding legibility - companies that are easy to value by analogy to public hyperscalers, easy to explain to LP boards, easy to justify as defensive positions - rather than funding breadth.

When 70% of all funding flows to rounds of $100 million or more, and seed funding is simultaneously contracting, venture capital is not spreading risk across the innovation economy. It is concentrating it inside a single thesis.[1]

The rounding error in this analysis is not the next large language model, which will get funded regardless. It is the climate startup that needed $8 million and a five-year horizon, the biotech that required patience before a clinical signal, the infrastructure company in an unglamorous vertical with no AI narrative to attach. Venture capital has always been a selective instrument. In 2025, its selectivity collapsed to a point where it is less a mechanism for allocating risk across the economy than a leveraged bet on one sector's ability to deliver returns before the LP base contracts further.

PitchBook: 41% of All VC Dollars Deployed in 2025 Have Gone to Just 10 Startups (paywalled; secondary access via SaaStr) Inline ↗

SiliconANGLE / PitchBook-NVCA Venture Monitor: AI Dominates Global Venture Capital as 2025 Deal Value Nears Record Inline ↗

Crunchbase: Why Top VCs Expect More Venture Dollars, Bigger Rounds, and Fewer Winners in 2026 Inline ↗